Get Pre-Approved: NH Mortgage Pre-Approval Explained

Get Pre-Approved: NH Mortgage Pre-Approval Explained

Embarking on the journey of buying a home in New Hampshire is an exciting prospect, but navigating the competitive housing market requires a strategic approach. One of the most critical initial steps you can take is obtaining mortgage pre-qualification to understand your eligibility for a mortgage. securing a mortgage pre-approval, a powerful tool that can significantly streamline your homeownership dreams. This guide will demystify the mortgage pre-approval process, offering insights tailored specifically for NH homebuyers.

Introduction

The Importance of Getting Pre-Approved in Today's NH Housing Market

In today's dynamic New Hampshire housing market, getting pre-approved for a mortgage is not just a recommendation; it's a necessity for anyone serious about shopping for a home. With demand often outpacing supply, sellers receive multiple offers, making a strong and confident bid essential. A mortgage pre-approval letter signals to sellers that you are a serious and qualified buyer, giving you a competitive edge in securing your perfect home and navigating the complex real estate landscape with greater ease.

Overview of Mortgage Pre-Approval

Mortgage pre-approval is a crucial step in the home buying process, signifying that a lender has reviewed your financial information and determined how much they are willing to loan you. This formal assessment provides a clear understanding of your potential loan amount, monthly payment, and what you can truly afford, setting a realistic budget for your home search. It is a vital component for anyone considering buying a home, especially first-time homebuyers in New Hampshire looking for favorable loan options.

What Is Mortgage Pre-Approval?

Definition of Mortgage Pre-Approval

Mortgage pre-approval is a formal commitment from a mortgage lender, indicating that you meet specific eligibility criteria for a mortgage loan up to a certain amount. This thorough review of your financial situation, including your credit score, debt-to-income ratio, and income, culminates in a pre-approval letter that confirms your eligibility for a mortgage. This letter empowers you to make an offer on a home with confidence, knowing you have a lender ready to back your financial commitment, solidifying your position as a serious and capable buyer in the NH market.

Difference Between Pre-Approval and Pre-Qualification

While often confused, mortgage pre-qualification and mortgage pre-approval serve distinct purposes in the process of shopping for a home. Pre-qualification is an informal estimate based on self-reported financial information, offering a rough idea of what you might be able to borrow. In contrast, pre-approval involves a firm commitment from the lender regarding the loan amount they are willing to provide. The table below highlights key differences between the two processes:

Feature Pre-Approval Credit Check Comprehensive (hard inquiry) Verification Financial documents verified

Why Pre-Approval Is the Most Important Step

Stronger Negotiating Power

Having a pre-approval letter significantly enhances your negotiating power when you make an offer on a home, as it demonstrates your readiness to borrow for a home. Sellers are more inclined to consider an offer from a buyer who has already been pre-approved by a lender, as it demonstrates financial readiness and shows sellers that you are serious about moving forward with the purchase. This can be particularly advantageous in a competitive market where multiple buyers are vying for the same property, allowing you to present a more compelling and confident proposal.

Establishing an Accurate Budget

One of the primary benefits of getting pre-approved for a mortgage is the establishment of an accurate budget. The pre-approval process clarifies the maximum loan amount you are able to borrow, along with an estimate of your potential monthly payment, closing costs, and even mortgage insurance if applicable. This detailed insight into your financial capacity prevents you from looking at properties beyond your reach, saving time and emotional energy during your home search, and allowing your real estate agent to show you homes within your actual budget.

Confidence for Sellers

A mortgage pre-approval instills significant confidence in sellers and shows sellers that you are a serious buyer, making your offer more appealing. When a seller receives an offer accompanied by a pre-approval letter, they know that a reputable lender has thoroughly vetted your financial situation, including your credit report and tax returns. This assurance dramatically reduces the uncertainty and potential delays associated with financing, making your offer stand out as solid and reliable, particularly in a hot market where sellers prioritize swift and secure transactions with qualified buyers.

How to Get Pre-Approved in New Hampshire

Step-by-Step Guide to the Pre-Approval Process

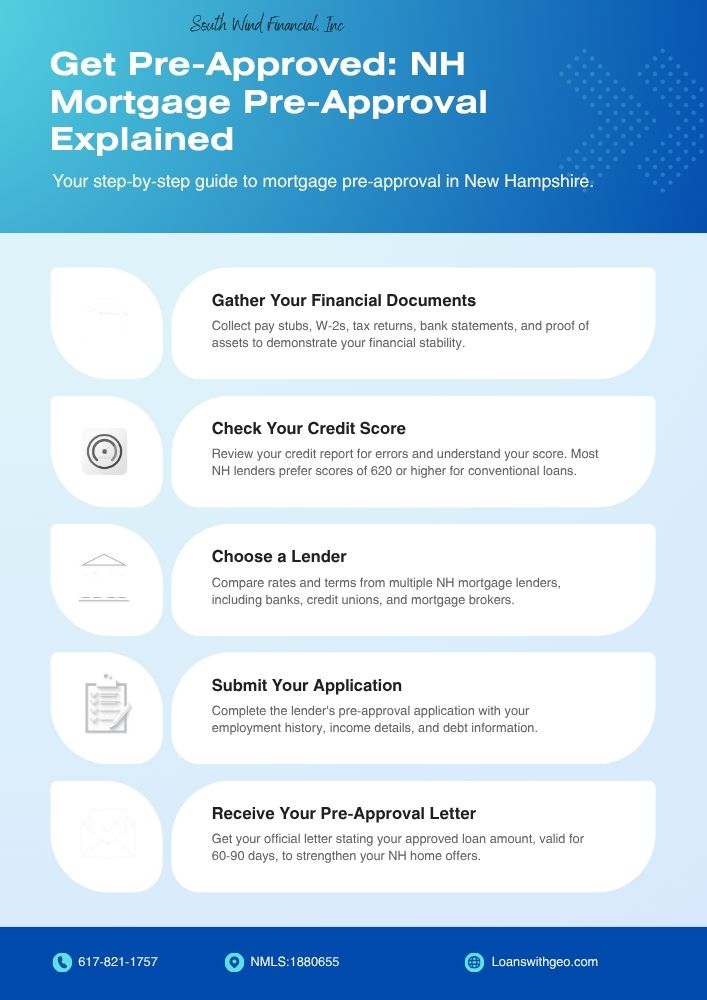

The mortgage pre-approval process in New Hampshire involves several key steps to ensure you secure the best home loan possible. These steps include:

Gathering all necessary financial documents, such as recent pay stubs, bank statements, and tax returns.

Completing a mortgage application, which allows your lender to perform a comprehensive credit check, assessing your credit score and financial history.

Having the lender review your overall financial situation to determine the maximum loan amount you are able to borrow and issue your pre-approval letter, empowering you to make an informed offer on a home.

Choosing the Right Mortgage Broker

Selecting the right mortgage broker is a crucial decision that can significantly impact your home buying journey in New Hampshire. An experienced mortgage broker will not only guide you through the intricacies of the pre-approval process but also help you compare various loan options and find competitive mortgage rates tailored to your financial situation. Look for a broker who is knowledgeable about local lending nuances, responsive, and committed to helping you achieve your homeownership dreams, ensuring a smooth transition into your perfect home.

Understanding Your Home Buying Journey

Understanding your home buying journey from the outset is essential for a stress-free experience, especially in New Hampshire's dynamic real estate market. Getting pre-approved for a mortgage is the foundational step, providing clarity on your budget and what you are truly able to borrow. This understanding empowers you to work effectively with your real estate agent, efficiently search for homes within your means, and confidently make an offer on a home, ultimately accelerating your path to homeownership.

Documents You'll Need

Checklist for NH Buyers

For NH buyers, preparing a comprehensive checklist of documents for mortgage pre-approval is vital for a smooth process. You will generally need to provide several key documents, including:

Recent pay stubs covering at least 30 days

Two years of W-2 forms or 1099s if self-employed

Two months of bank statements for all accounts

Two years of federal tax returns

Additionally, be prepared to provide documentation for any other assets or debts, ensuring your lender has a complete picture of your financial situation to accurately assess your mortgage loan eligibility.

Common Documentation Requirements

Beyond the basics, common documentation requirements for mortgage pre-approval often include proof of identity, such as a driver's license or passport, and details about your current and past employment history. If you are self-employed, you may need to provide profit and loss statements. For those with significant assets, investment account statements will also be necessary. Providing these financial documents upfront allows your lender to conduct a thorough credit check and determine your debt-to-income ratio, which are critical factors in the pre-approval process for your home loan.

Factors That Affect Your Pre-Approval

Impact of Credit Score

Your credit score plays a pivotal role in the mortgage pre-approval process, directly influencing the loan amount you are able to borrow and the mortgage rates you'll be offered. A strong credit score signals to the lender that you are a responsible borrower, making you eligible for more favorable loan terms and potentially a lower monthly payment, which can help you secure a low mortgage. Conversely, a lower credit score might result in higher interest rates or even a denial of your mortgage loan, emphasizing the importance of a healthy credit report.

Understanding Debt-to-Income Ratio

The debt-to-income ratio (DTI) is a critical factor lenders evaluate during the pre-approval process, as it reflects your ability to manage monthly payments and take on additional debt. This ratio compares your total monthly debt obligations to your gross monthly income. A lower DTI indicates that you have more disposable income available to cover a mortgage payment, making you a less risky borrower in the eyes of the lender and increasing your chances of getting pre-approved for a mortgage.

Importance of Down Payment and Employment History

Your down payment and employment history are significant components that directly affect your mortgage pre-approval. A larger down payment demonstrates financial stability and can result in more favorable loan terms, potentially reducing your monthly payment and eliminating the need for private mortgage insurance. Similarly, a stable and consistent employment history, typically two years with the same employer, reassures the lender of your reliable income source, which is crucial for getting approved for a mortgage loan and securing your dream of homeownership.

NH-Specific Considerations

Local Lending Nuances

When seeking mortgage pre-approval in New Hampshire, it’s important to be aware of local lending nuances that might affect your home loan. Property taxes can vary significantly by town, impacting your overall monthly payment, so understanding these local differences is crucial. An experienced mortgage broker familiar with the NH market can provide invaluable insights into specific community regulations and potential zoning considerations that could influence your purchase, ensuring a smoother mortgage process.

State Programs and Incentives for First-Time Homebuyers

New Hampshire offers various state programs and incentives designed to assist first-time homebuyers in achieving homeownership. These programs often include favorable loan options, down payment assistance, or reduced mortgage rates, making it easier to get pre-approved for a mortgage. It's essential to discuss these specific programs with your lender or mortgage broker during the pre-approval process to see if you qualify, as they can significantly reduce your financial burden and help you secure your perfect home in NH.

Common Mistakes to Avoid

Misunderstanding Pre-Approval vs. Pre-Qualification

A common mistake many aspiring homeowners make is confusing mortgage pre-approval with mortgage pre-qualification, which can lead to significant setbacks in the home buying process and affect their eligibility for a mortgage. While pre-qualification offers a preliminary estimate of what you might be able to borrow based on self-reported financial information, it lacks the formal verification of a hard credit check and review of financial documents. Sellers and real estate agents in NH recognize this distinction, valuing a robust pre-approval letter that demonstrates a lender's commitment and your financial readiness to make an offer on a home.

Fear of Credit Impact

Another prevalent concern that can hinder individuals from pursuing mortgage pre-approval is the fear of a negative impact on their credit score due to the necessary credit check, which is essential for determining their eligibility for a mortgage. While a hard credit inquiry, which is part of the pre-approval process, does temporarily affect your credit report, the impact is usually minimal, often just a few points. The benefits of getting pre-approved for a mortgage, such as gaining a clear understanding of your loan amount and increasing seller confidence, far outweigh this slight, short-term dip, especially when you are serious about buying a home.

Expert Tips for Successful Pre-Approval

How to Prepare Financially

To ensure a successful mortgage pre-approval, proactive financial preparation is paramount. Begin by reviewing your credit report for any inaccuracies and dispute them promptly to maintain a healthy credit score, which is crucial for your mortgage pre-qualification and pre-approval. Focus on reducing your debt-to-income ratio by paying down existing debts and avoid taking on new lines of credit. Consistently save for a substantial down payment and keep your financial documents, such as recent pay stubs and bank statements, organized and readily accessible to streamline the pre-approval process.

Building a Relationship with Your Mortgage Broker

Cultivating a strong relationship with your mortgage broker is an invaluable expert tip for a smooth and successful mortgage pre-approval, especially when considering options like an FHA loan. A dedicated mortgage broker, like LoansWithGeo, acts as your advocate, guiding you through every step of the mortgage process, from gathering financial information to securing the best loan options and mortgage rates. Open communication and trust with your broker ensure they understand your financial situation, helping you navigate any challenges and ultimately get approved for a mortgage that aligns with your homeownership goals in NH.

What Happens After Pre-Approval

Next Steps in the Home Buying Process

Once you've successfully obtained your mortgage pre-approval, the exciting next steps in the home buying process begin. With your pre-approval letter in hand, your real estate agent can confidently show you homes within your established budget, allowing you to focus on finding your next home. You are now empowered to make an offer on a home, knowing precisely what loan amount you are able to borrow. This crucial step streamlines negotiations, gives sellers confidence, and significantly shortens the time from offer acceptance to closing, moving you closer to your perfect home in NH.

Maintaining Your Pre-Approval Status

Maintaining your mortgage pre-approval status is critical throughout your home buying journey. It is essential to avoid making any significant financial changes, such as taking on new debt, making large purchases, or changing employment, as these actions can negatively impact your debt-to-income ratio or credit score. Your lender will re-verify your financial information before closing, so preserving the financial situation that secured your initial pre-approval ensures a smooth transition to your home loan and helps you get approved for a mortgage without last-minute complications.

Conclusion

Encouragement to Get Pre-Approved

The journey to homeownership in New Hampshire is an exciting adventure, and getting pre-approved for a mortgage is undeniably the most important first step. This crucial process not only provides a clear understanding of your financial capacity and the loan amount you are able to borrow but also equips you with the confidence and credibility to make a competitive offer on a home. Embrace this empowering step to streamline your home buying process and move closer to securing your perfect home with peace of mind.

Call to Action: Contact LoansWithGeo for Personalized Pre-Approval

Ready to take the most important step towards buying a home in New Hampshire? Don't navigate the mortgage pre-approval process alone. Contact South Wind Financial, MB #9462, LoansWithGeo.com today for personalized guidance and expert assistance in securing your mortgage pre-approval. Our dedicated team is committed to helping you understand your loan options and achieve your homeownership dreams. Reach out to us at [email protected], call or text us at 617-821-1757, or connect with our NMLS #1880655. Se habla español.