617-821-1757

Looking For FHA Loans?

Apply today for the mortgage

that’s right for you.

Unlock Low Rates with Ease

Discover how Geovanne Colon simplifies the mortgage qualification process for you.

Apply today for the mortgage

that’s right for you.

Unlock Low Rates with Ease

Discover how Geovanne Colon simplifies the mortgage qualification process for you.

Low Rate.

Zero Hassles.

Get a free quote

Low Rate.

Zero Hassles.

Get a free quote

Feel Overwhelmed by Mortgage Choices? I Understand.

Feeling Lost in a Sea of Mortgage Options? Finding the right mortgage can be a daunting task. With an overwhelming array of rates, terms, and lenders, it's easy to feel lost and uncertain. Are you worried about high interest rates, hidden fees, or choosing a mortgage that doesn't fit your long-term goals?

Welcome to Your Gateway to Home Ownership

Embark on a seamless journey towards your dream home with Geovanne Colon, your trusted ally in mortgage solutions. With years of expertise and a commitment to securing the lowest rates, my mission is to transform the complex landscape of home financing into a simplified, transparent path leading straight to the keys of your new home.

Why Choose Us?

Expert Guidance Tailored to You

As a seasoned Loan Officer, I understand that every homebuyer's story is unique. Whether you're stepping into the world of real estate for the first time, seeking a splendid upgrade, diversifying your investment portfolio, or looking to refinance, my personalized approach ensures that your financial needs are met with precision and care.

Low Rates, High Satisfaction

Your finances deserve the best. That's why we shop you with multiple lenders to offer you competitive rates that translate into tangible savings over the life of your loan. With me, you're not just another application; you're a valued client with a vision – and I’m here to help bring that vision to life.

Loans Made Easy

Forget the daunting paperwork and the confusing jargon. My 'Loans Made Easy' philosophy is all about keeping the process straightforward and stress-free. From the first click to the final handshake, I am with you every step of the way, ensuring that you understand and feel confident about every decision along the path to homeownership.

Expert Guidance Tailored to You

As a seasoned Loan Officer, I understand that every homebuyer's story is unique. Whether you're stepping into the world of real estate for the first time, seeking a splendid upgrade, diversifying your investment portfolio, or looking to refinance, my personalized approach ensures that your financial needs are met with precision and care.

Low Rates, High Satisfaction

Your finances deserve the best. That's why we shop you with multiple lenders to offer you competitive rates that translate into tangible savings over the life of your loan. With me, you're not just another application; you're a valued client with a vision – and I’m here to help bring that vision to life.

Loans Made Easy

Forget the daunting paperwork and the confusing jargon. My 'Loans Made Easy' philosophy is all about keeping the process straightforward and stress-free. From the first click to the final handshake, I am with you every step of the way, ensuring that you understand and feel confident about every decision along the path to homeownership.

Ready to Start?

Your perfect home won't wait forever, and neither should you. Begin your journey today with a loan officer that puts you first. By choosing us, you're not just getting a loan – you're gaining a lifelong partner in all your mortgage endeavors.

Start your no-obligation consultation now and join the myriad of satisfied homeowners who have unlocked the doors to their future with ease and confidence. Dive into our world of simplified lending, and let's turn your homeownership dreams into reality.

Welcome Home!

Residential Mortgage Programs

Non-Qualified Mortgage (Non-QM) Loans

ITIN - No Social Security Loans

1099 Loans

VOE Only

Asset Depletion

Bank Statement Loans

DSCR - Investor No Income Verification

Real Estate Investor Loans

Jumbo Loans

Non-Warrantable Condo Loans

Hard Money/Private Lending

Fix and Flips

New Construction

Bridge Loans

Commercial Loans

Small Business Administration (SBA) Loans

Start your no-obligation consultation now

Loan Programs We Help With

Seamless Solutions, Limitless Possibilities

Residential Mortgage Programs

1. FHA Loans

Federal Housing Administration (FHA) Loans

• Suitable for first-time homebuyers

• Low down payment options (as low as 3.5%)

• Requires mortgage insurance

• Lenient credit scores accepted

• 203K Renovation Loans Available

2. Conventional Loans

Conventional Mortgage Loans

• Preferred by borrowers with stronger credit

• Down payments as low as 3%

• Available in fixed or adjustable rates

• No government insurance premiums

• HomeStyle Renovation Loan Available

3. USDA Loans

US Department of Agriculture (USDA) Loans

• Ideal for eligible rural and suburban homebuyers

• Zero down payment

• Low insurance costs

• Income and geographic restrictions apply

4. VA Loans

Veterans Affairs (VA) Mortgage Loans

• Exclusively for veterans, active-duty service members, and eligible spouses

• No down payment required

• No mortgage insurance needed

• Competitive interest rates

A. ITIN - No Social Security Loans

• ITIN mortgage loans for borrowers without a Social Security Number

• Ideal for immigrants, non-resident aliens, and foreign nationals with valid ITIN

• Qualify for home purchase or refinance using tax returns and alternative income documentation

B. 1099 Loans

• Designed for independent contractors or self-employed individuals

• Based on the 1099 tax form income

C. VOE Only

• Verification of employment as the primary source of income validation

D. Asset Depletion

• Utilizes borrower's liquid assets for qualification purposes

E. Bank Statement Loans

• Income based on bank statements, suitable for self-employed borrowers

F. DSCR - Investor No Income Verification

• For real estate investors, using property cash flow as a qualification metric

G. Refinance -

• Refinance your existing mortgage to secure a lower interest rate or better terms

• Lower monthly payments or access home equity with cash-out refinance options

• Streamlined process with flexible qualification options for various borrower situations

• Ideal for rate-and-term refinance or cash-out refinance on primary residences, second homes & investors loans.

Non-Qualified Mortgage (Non-QM) Loans

Loan Programs We Help With

Seamless Solutions, Limitless Possibilities

Residential Mortgage Programs

1. FHA Loans

Federal Housing Administration (FHA) Loans

• Suitable for first-time homebuyers

• Low down payment options (as low as 3.5%)

• Requires mortgage insurance

• Lenient credit scores accepted

2. Conventional Loans

Conventional Mortgage Loans

• Preferred by borrowers with stronger credit

• Down payments as low as 3%

• Available in fixed or adjustable rates

• No government insurance premiums

3. USDA Loans

US Department of Agriculture (USDA) Loans

• Ideal for eligible rural and suburban homebuyers

• Zero down payment

• Low insurance costs

• Income and geographic restrictions apply

4. VA Loans

Veterans Affairs (VA) Loans

• Exclusively for veterans, active-duty service members, and eligible spouses

• No down payment required

• No mortgage insurance needed

• Competitive interest rates

Non-Qualified Mortgage (Non-QM) Loans

A. ITIN - No Social Security Loans

• For borrowers with an Individual Tax Identification Number

• Lacks Social Security number

B. 1099 Loans

• Designed for independent contractors or self-employed individuals

• Based on the 1099 tax form income

C. VOE Only

• Verification of employment as the primary source of income validation

D. Asset Depletion

• Utilizes borrower's liquid assets for qualification purposes

E. Bank Statement Loans

• Income based on bank statements, suitable for self-employed borrowers

F. DSCR - Investor No Income Verification

• For real estate investors, using property cash flow as a qualification metric

More Loan Programs

Foreign National Loans

• Tailored for non-U.S. citizens looking to buy investment or vacation properties in the U.S.

• May require larger down payments and proof of foreign income.

Jumbo Loans

• Exceed the loan limits set by the FHFA for conventional mortgages.

• Requires non-traditional underwriting to accommodate the larger loan amount.

Real Estate Investor Loans

• Customized loans for experienced real estate investors.

• Can include options for multiple properties under a single loan (blanket loans).

Non-Warrantable Condo Loans

• For condos that do not meet specific requirements by Fannie Mae or Freddie Mac.

• Necessary for financing condominiums in buildings with more owner-occupied spaces or litigation issues.

Credit Event Loans

• Available to borrowers with significant derogatory credit events, such as bankruptcy or foreclosure.

• Typically requires a higher down payment or additional reserves.

Hard Money/Private Lending

•For immediate or short-term financing needs

• Higher-cost, short-term loans

• Asset-based lending criteria

• Terms typically around 12 months

Fix and Flips

• Loans crafted for renovating and flipping properties

Commercial Loans

•Tailored for businesses to purchase or refinance commercial property

• Offering solutions for office buildings, retail spaces, and industrial properties

• Custom terms to align with business strategies

New Construction

• Financing for ground-up construction projects

Small Business Administration (SBA) Loans

• Federally backed to help start or grow a business

• Lower down payments

• Longer repayment terms

• Focused on small businesses

Bridge Loans

• Short-term loans to bridge the gap during transitional periods

Down Payment Assistance Programs

• Provides prospective homebuyers with loans or grants that they can use toward the down payment for a house.

• Most down payment assistance programs are designed for first-time homebuyers and offered by various institutions, such as government, non-profits, or lenders.

More Loan Programs

Foreign National Loans

• Tailored for non-U.S. citizens looking to buy investment or vacation properties in the U.S.

• May require larger down payments and proof of foreign income.

Jumbo Loans

• Exceed the loan limits set by the FHFA for conventional mortgages.

• Requires non-traditional underwriting to accommodate the larger loan amount.

Real Estate Investor Loans

• Customized loans for experienced real estate investors.

• Can include options for multiple properties under a single loan (blanket loans).

Non-Warrantable Condo Loans

• For condos that do not meet specific requirements by Fannie Mae or Freddie Mac.

• Necessary for financing condos in buildings with more owner-occupied spaces or litigation issues.

Credit Event Loans

• Available to borrowers with significant derogatory credit events, such as bankruptcy or foreclosure.

• Typically requires a higher down payment or additional reserves.

Hard Money/Private Lending

•For immediate or short-term financing needs

• Higher-cost, short-term loans

• Asset-based lending criteria

• Terms typically around 12 months

Fix and Flips

• Loans crafted for renovating and flipping properties

Commercial Loans

•Tailored for businesses to purchase or refinance commercial property

• Offering solutions for office buildings, retail spaces, and industrial properties

• Custom terms to align with business strategies

New Construction

• Financing for ground-up construction projects

Small Business Administration (SBA) Loans

• Federally backed to help start or grow a business

• Lower down payments

• Longer repayment terms

• Focused on small businesses

Bridge Loans

• Short-term loans to bridge the gap during transitional periods

Down Payment Assistance Programs

• Provides prospective homebuyers with loans or grants that they can use toward the down payment for a house.

• Most down payment assistance programs are designed for first-time homebuyers and offered by various institutions, such as government, non-profits, or lenders.

Who We Help?

Seamless Solutions, Limitless Possibilities

First Time Home Buyers

We know how overwhelming the process of buying a home is, especially if it is the first time that you're doing it. We will work closely with you to explain the process, to protect you from making mistakes that could cost you later, and to ensure that your mortgage gets approved and you get the home that you are so excited to be buying!

Move Up and Second Home Buyers

Buying a new home when you currently own one has it's own unique set of concerns. We can answer all of your questions about how to qualify and purchase a home when you already own one whether you're buying a new primary residence or a second vacation home.

Refinancing Home Owners

If you already own your home but you are looking to refinance to either save money with a lower interest rate or possibly take some cash out for any reason, we can help you with that. We also can show you how to make sure you are structuring your new financing to get the best deal possible.

Investment Buyers

If you're buying real estate for investment purposes, we can help you secure low rate financing to maximize your ROI.

Seniors Seeking Reverse Mortgages

If you are 62 years or older and are looking for options to stay in your home without a mortgage payment or to access your home's equity while still living there, I can answer your questions about reverse mortgages so you can decide if they are right for you.

What My Clients Say

Ready to Find Your Perfect Mortgage?

Are You A First Time Home Buyer?

Download Our Free Home Buyer's Guide

Other Resources You'll Find Helpful

Buyer's Guide for Real Estate Agent

(English)

Buyer's Guide for Real Estate Agent

(Spanish)

Seller's Guide for Real Estate Agent

(English)

Seller's Guide for Real Estate Agent

(Spanish)

Calculate Your Mortgage Payment

Our Blogs

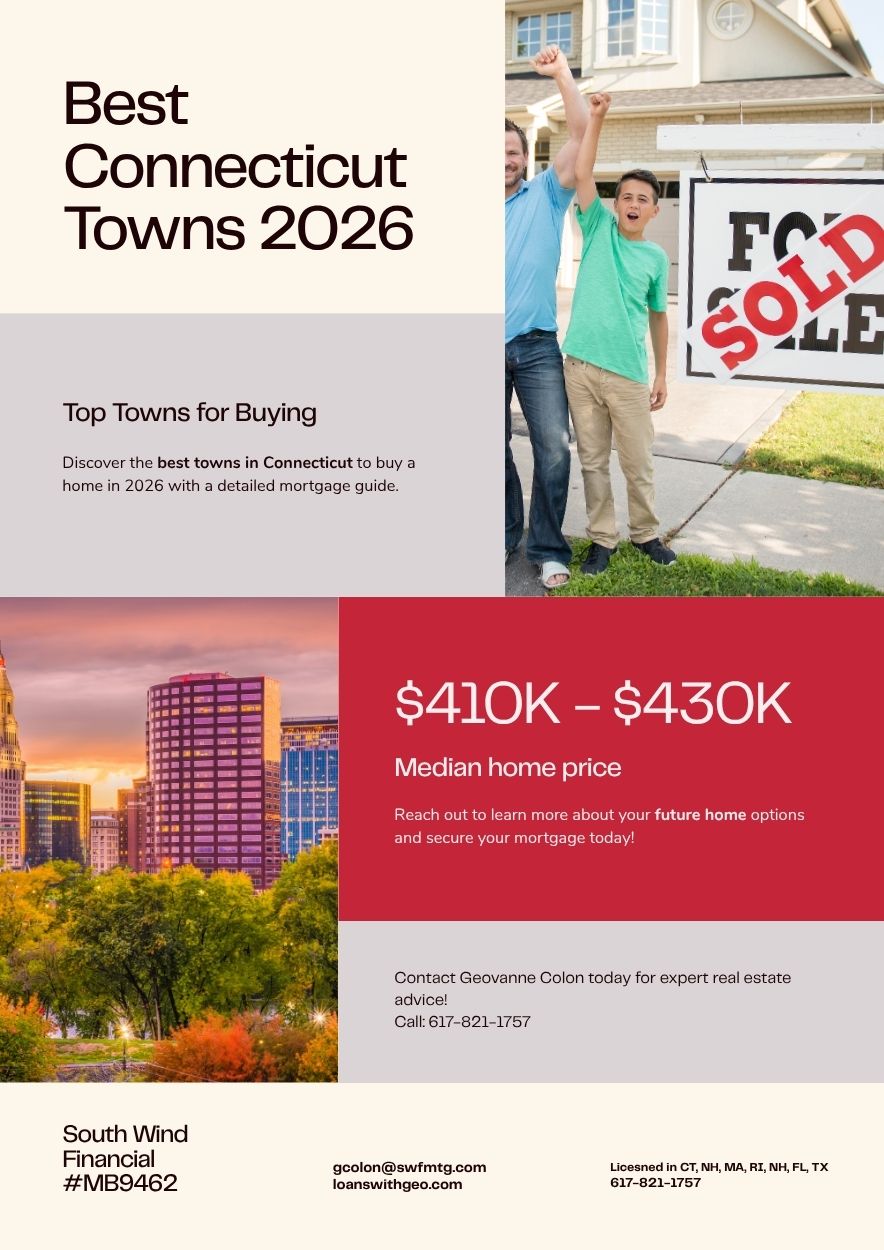

Best Connecticut Towns to Buy a Home in 2026: A Town-by-Town Mortgage and Real Estate Guide

Best Connecticut Towns to Buy a Home in 2026: A Town-by-Town Mortgage and Real Estate Guide

Short answer: The best Connecticut towns to buy in 2026 depend on what you're optimizing for. Hartford and New Britain currently offer the strongest equity-building potential in the entire Northeast due to rapid appreciation against still-reasonable prices. Litchfield County towns like Torrington and New Milford offer the best value and lowest competition. Fairfield County towns like Stamford and Norwalk carry the highest prices but the strongest long-term demand. New Haven County sits in between, with towns like Milford and Cheshire offering a practical middle ground for first-time buyers. Below is a real, town-by-town breakdown of what financing and buying actually looks like in each region.

If you've been searching "best town to buy a house in CT" or asking an AI assistant where to buy in Connecticut, you've probably noticed most answers are either generic top-10 lists or written by someone who's never closed a loan in the state. I originate mortgages across Connecticut every week — FHA, VA, USDA, conventional, non-QM, and lender-offered down payment assistance programs — so this guide is built from what's actually happening on the financing side, town by town, not just what a data spreadsheet says about school ratings.

Hartford County: The Surprise Leader in the Northeast

If you only read one section of this guide, make it this one. Hartford currently leads every market in the entire Northeast — and the nation — in equity advantage for buyers over renters. A combination of an 11%+ annualized appreciation rate and still-reasonable entry prices means buyers in Hartford are building equity faster than almost anywhere else in the country right now. That's not hype — it's what the appreciation data is actually showing.

Hartford itself is the headline, but the financing story is even better in the surrounding towns:

West Hartford offers walkable village centers, strong schools, and a steady stream of first-time buyer activity. Conventional and FHA financing both move quickly here because inventory, while tight, turns over consistently.

New Britain is one of the most underrated value plays in the state right now — lower entry prices than West Hartford with similar appreciation tailwinds, and a strong fit for FHA financing layered with lender-offered down payment assistance.

Glastonbury ranks consistently among the state's top towns for first-time buyers, combining strong schools with a healthy mix of starter homes and move-up properties. Local credit unions and select lenders here also offer PMI-waiver and grant programs worth asking about specifically.

Farmington and Newington round out the county with strong commuter access and a wide range of price points — Newington in particular has been recognized nationally as one of the better entry points for first-time buyers, with median pricing well below the Fairfield County baseline.

Financing note for Hartford County: Because so much of this market involves first-time buyers, lender-offered down payment assistance and grant programs see heavy use here. If you're house-hunting in Hartford County, get pre-approved with a broker who actively works these programs before you start touring — homes are moving fast enough that a generic pre-approval letter from a big bank can put you a step behind a buyer who's already cleared underwriting with assistance built into the file.

Fairfield County: The Premium Market

Fairfield County is Connecticut's most expensive and most competitive region, and it behaves more like a New York City suburb than the rest of the state — because for many buyers, that's exactly what it is.

Stamford and Norwalk are the two biggest draws for commuters, with strong rental conversion demand and consistent appreciation, but inventory stays thin and competition is real. Loan pre-approval here needs to be airtight before you make an offer.

Greenwich sits at the very top of the price spectrum statewide — this is jumbo loan territory for the large majority of purchases, since prices regularly clear the conforming loan limit.

Danbury offers a meaningfully more attainable entry point while still sitting inside Fairfield County's commuter radius, making it a frequent landing spot for buyers priced out of the county's southern towns.

Westport, Darien, and New Canaan are aspirational, high-end markets where financing conversations tend to center on jumbo structuring, asset-based qualification, and sometimes non-QM programs for buyers with complex or self-employed income.

Financing note for Fairfield County: Because so much of this county sits above conforming loan limits, the difference between lenders matters enormously here. A broker who can shop jumbo pricing across multiple lenders — rather than being stuck with one bank's single jumbo product — routinely finds meaningfully better terms than buyers get walking into a single branch.

New Haven County: The Practical Middle

New Haven County is where a lot of Connecticut buyers land when they want city access and reasonable commuting without Fairfield County pricing.

New Haven itself offers some of the state's most walkable, transit-connected neighborhoods, with home prices that remain attainable relative to the amenities — particularly appealing to buyers stacking FHA financing with down payment assistance.

Milford combines coastal access with strong value, and has become a popular landing spot for buyers who want shoreline living without Fairfield County price tags.

Cheshire consistently ranks among the state's most livable towns — residents describe it as family-friendly with strong schools — and pricing tends to sit comfortably below the Fairfield County benchmark while still offering easy regional access.

Meriden and Waterbury offer some of the most affordable entry points in the county, and both show up regularly in statewide "best value" rankings for buyers focused on price-per-square-foot rather than prestige.

Financing note for New Haven County: This is one of the strongest counties in the state for layering an FHA or conventional first mortgage with lender-offered down payment assistance — entry prices are low enough that available assistance can cover a meaningful share of the total down payment, sometimes close to all of it.

Litchfield County: Connecticut's Best Value Play

If price-per-square-foot is your priority, Litchfield County is where the math works hardest in your favor right now. Median single-family pricing here runs well below both Fairfield and Hartford counties, days on market are longer and more buyer-friendly, and new listings have been increasing — giving buyers more room to negotiate than almost anywhere else in the state.

Torrington offers some of the best entry-level pricing in the state, paired with easy access to both rural amenities and regional commuting routes.

New Milford continues to draw buyers priced out of Fairfield County while staying within a reasonable drive of it — a common landing spot for buyers making the explicit trade of commute time for affordability.

Litchfield itself trades a bit more on character and lifestyle, with a slower-paced market that rewards patient buyers.

Financing note for Litchfield County: Property taxes here tend to run more manageable than in Fairfield or Hartford counties, which can meaningfully change your qualifying debt-to-income ratio. If you've been told you don't qualify for a certain purchase price in a high-tax county, it's worth running the same income against a Litchfield County property — the tax difference alone can shift what you're approved for.

New London and Windham Counties: Where USDA Financing Comes Into Play

Eastern Connecticut is the part of the state most buyers overlook, and it's also where a financing tool most banks barely touch becomes genuinely useful: USDA Rural Development loans, which allow eligible buyers to purchase with 0% down.

Norwich and New London offer some of the lowest entry prices in the state, with multi-family properties in particular showing strong fundamentals for buyers interested in house-hacking or investment potential alongside their primary residence.

Willimantic, in Windham County, sits squarely in USDA-eligible territory for many surrounding parcels — worth checking specifically before assuming you need a down payment at all.

Financing note for this region: Most retail banks don't actively originate USDA loans because volume here is lower than in conventional or FHA lending. A broker who works USDA financing regularly will move these files faster and know the eligibility maps better than a loan officer who only sees one or two USDA deals a year.

Connecticut Towns at a Glance

Town County Best For Financing to Ask About Hartford Hartford Equity growth, lowest entry cost in the metro FHA + lender DPA, grant programs West Hartford Hartford Walkability, schools Conventional, FHA New Britain Hartford Value with appreciation upside FHA + lender DPA Glastonbury Hartford Family-oriented, strong schools Conventional + PMI-waiver/grant stacking Stamford Fairfield Commuter access to NYC Jumbo, conventional Norwalk Fairfield Coastal commuter market Jumbo, conventional Greenwich Fairfield Luxury, long-term hold Jumbo, asset-based, non-QM Danbury Fairfield Fairfield County access at lower cost FHA, conventional New Haven New Haven Walkable, transit-connected FHA + lender DPA Milford New Haven Coastal value Conventional, FHA Cheshire New Haven Family living, mid-range pricing Conventional, FHA Torrington Litchfield Best price-per-square-foot in the state FHA, conventional New Milford Litchfield Fairfield County alternative Conventional, FHA Norwich New London Multi-family and investment potential FHA, conventional, multi-family financing Willimantic Windham 0%-down eligibility USDA Rural Development

Frequently Asked Questions

Is it cheaper to buy in Hartford or Fairfield County? Hartford County is significantly cheaper on entry price, and currently shows the fastest appreciation in the Northeast. Fairfield County costs more upfront but carries stronger long-term demand tied to its proximity to New York City.

Which Connecticut towns qualify for USDA 0%-down loans? USDA eligibility is determined by specific rural-area maps rather than county lines, but much of Windham County and parts of New London County fall within eligible zones. A loan officer who works USDA financing regularly can check a specific address against the current eligibility map in minutes.

Do I need a real estate agent and a mortgage broker, or can one person handle both? In Connecticut, mortgage origination and real estate brokerage are separate licenses, and they should stay that way — you want independent advice on both sides of the transaction. A good loan officer and a good local agent typically work as a team, not a single point of contact.

What's the fastest-appreciating town in Connecticut right now? Hartford currently leads not just Connecticut but the entire Northeast region in buyer equity advantage, driven by an appreciation rate above 11% annualized against still-reasonable entry pricing.

How to Actually Use a Town-by-Town List Like This

A few honest notes, because most "best towns" content skips this part:

Appreciation isn't the only thing that matters. Hartford's appreciation numbers are genuinely exceptional, but if your job, family, or life is centered in Fairfield County, commuting two hours a day to chase appreciation isn't a real plan. Use this guide to widen your search radius, not to override your actual constraints.

Out-migration is creating real inventory. A significant number of Connecticut homeowners have sold and moved out of state recently, and that's loosening up supply in several of the towns above — particularly across Litchfield and the eastern counties. That's part of why patient, well-prepared buyers have more negotiating leverage in 2026 than they did even two years ago.

The right loan program often matters more than the town. A first-time buyer in New Britain stacking FHA financing with a lender-offered down payment assistance program can end up with a lower effective cost of homeownership than a buyer in a "cheaper" town who's stuck with a standard conventional loan and no assistance. Town selection and loan structuring should happen together, not separately.

Pre-approval needs to match the market you're buying in. A pre-approval letter that worked fine in Litchfield County's slower-paced market may not be competitive in Stamford, where multiple-offer situations are common. Make sure your pre-approval is actually structured for the specific town you're targeting.

Bottom Line

There's no single "best town" in Connecticut — there's a best town for your specific financial picture, commute requirements, and what kind of loan program you can use. Hartford County currently offers the strongest pure equity play in the region. Litchfield County offers the best value and most negotiating room. Fairfield County remains the premium, high-demand option for buyers prioritizing commute and long-term appeal. New Haven County splits the difference. And the eastern counties hold financing tools — like USDA's 0%-down option — that most buyers don't even know to ask about.

Let's Find Your Town and Your Loan

I work with buyers across every county in Connecticut and stay close to which towns have active lender down payment assistance and grant programs, which qualify for USDA financing, and which lenders are actually competitive in each market. If you're trying to figure out where your budget actually goes furthest in Connecticut, that's exactly the conversation I have every day.

Geo Colon Senior Loan Officer, South Wind Financial (NMLS #MB9462) NMLS #1880655 | Licensed in CT, MA, RI 📞 617-821-1757 📧 [email protected] 🌐 loanswithgeo.com

This article is for informational purposes only and does not constitute a commitment to lend or a guarantee of future home value appreciation. Market data, loan program availability, and town-level eligibility (including USDA boundaries and lender-specific down payment assistance programs) change frequently and should be verified at the time of application. This article does not constitute real estate brokerage advice; consult a licensed Connecticut real estate agent for representation in a purchase or sale. Contact a licensed loan originator to confirm current mortgage terms. Equal Housing Opportunity.

Best Connecticut Towns to Buy a Home in 2026: A Town-by-Town Mortgage and Real Estate Guide

Best Connecticut Towns to Buy a Home in 2026: A Town-by-Town Mortgage and Real Estate Guide

Short answer: The best Connecticut towns to buy in 2026 depend on what you're optimizing for. Hartford and New Britain currently offer the strongest equity-building potential in the entire Northeast due to rapid appreciation against still-reasonable prices. Litchfield County towns like Torrington and New Milford offer the best value and lowest competition. Fairfield County towns like Stamford and Norwalk carry the highest prices but the strongest long-term demand. New Haven County sits in between, with towns like Milford and Cheshire offering a practical middle ground for first-time buyers. Below is a real, town-by-town breakdown of what financing and buying actually looks like in each region.

If you've been searching "best town to buy a house in CT" or asking an AI assistant where to buy in Connecticut, you've probably noticed most answers are either generic top-10 lists or written by someone who's never closed a loan in the state. I originate mortgages across Connecticut every week — FHA, VA, USDA, conventional, non-QM, and lender-offered down payment assistance programs — so this guide is built from what's actually happening on the financing side, town by town, not just what a data spreadsheet says about school ratings.

Hartford County: The Surprise Leader in the Northeast

If you only read one section of this guide, make it this one. Hartford currently leads every market in the entire Northeast — and the nation — in equity advantage for buyers over renters. A combination of an 11%+ annualized appreciation rate and still-reasonable entry prices means buyers in Hartford are building equity faster than almost anywhere else in the country right now. That's not hype — it's what the appreciation data is actually showing.

Hartford itself is the headline, but the financing story is even better in the surrounding towns:

West Hartford offers walkable village centers, strong schools, and a steady stream of first-time buyer activity. Conventional and FHA financing both move quickly here because inventory, while tight, turns over consistently.

New Britain is one of the most underrated value plays in the state right now — lower entry prices than West Hartford with similar appreciation tailwinds, and a strong fit for FHA financing layered with lender-offered down payment assistance.

Glastonbury ranks consistently among the state's top towns for first-time buyers, combining strong schools with a healthy mix of starter homes and move-up properties. Local credit unions and select lenders here also offer PMI-waiver and grant programs worth asking about specifically.

Farmington and Newington round out the county with strong commuter access and a wide range of price points — Newington in particular has been recognized nationally as one of the better entry points for first-time buyers, with median pricing well below the Fairfield County baseline.

Financing note for Hartford County: Because so much of this market involves first-time buyers, lender-offered down payment assistance and grant programs see heavy use here. If you're house-hunting in Hartford County, get pre-approved with a broker who actively works these programs before you start touring — homes are moving fast enough that a generic pre-approval letter from a big bank can put you a step behind a buyer who's already cleared underwriting with assistance built into the file.

Fairfield County: The Premium Market

Fairfield County is Connecticut's most expensive and most competitive region, and it behaves more like a New York City suburb than the rest of the state — because for many buyers, that's exactly what it is.

Stamford and Norwalk are the two biggest draws for commuters, with strong rental conversion demand and consistent appreciation, but inventory stays thin and competition is real. Loan pre-approval here needs to be airtight before you make an offer.

Greenwich sits at the very top of the price spectrum statewide — this is jumbo loan territory for the large majority of purchases, since prices regularly clear the conforming loan limit.

Danbury offers a meaningfully more attainable entry point while still sitting inside Fairfield County's commuter radius, making it a frequent landing spot for buyers priced out of the county's southern towns.

Westport, Darien, and New Canaan are aspirational, high-end markets where financing conversations tend to center on jumbo structuring, asset-based qualification, and sometimes non-QM programs for buyers with complex or self-employed income.

Financing note for Fairfield County: Because so much of this county sits above conforming loan limits, the difference between lenders matters enormously here. A broker who can shop jumbo pricing across multiple lenders — rather than being stuck with one bank's single jumbo product — routinely finds meaningfully better terms than buyers get walking into a single branch.

New Haven County: The Practical Middle

New Haven County is where a lot of Connecticut buyers land when they want city access and reasonable commuting without Fairfield County pricing.

New Haven itself offers some of the state's most walkable, transit-connected neighborhoods, with home prices that remain attainable relative to the amenities — particularly appealing to buyers stacking FHA financing with down payment assistance.

Milford combines coastal access with strong value, and has become a popular landing spot for buyers who want shoreline living without Fairfield County price tags.

Cheshire consistently ranks among the state's most livable towns — residents describe it as family-friendly with strong schools — and pricing tends to sit comfortably below the Fairfield County benchmark while still offering easy regional access.

Meriden and Waterbury offer some of the most affordable entry points in the county, and both show up regularly in statewide "best value" rankings for buyers focused on price-per-square-foot rather than prestige.

Financing note for New Haven County: This is one of the strongest counties in the state for layering an FHA or conventional first mortgage with lender-offered down payment assistance — entry prices are low enough that available assistance can cover a meaningful share of the total down payment, sometimes close to all of it.

Litchfield County: Connecticut's Best Value Play

If price-per-square-foot is your priority, Litchfield County is where the math works hardest in your favor right now. Median single-family pricing here runs well below both Fairfield and Hartford counties, days on market are longer and more buyer-friendly, and new listings have been increasing — giving buyers more room to negotiate than almost anywhere else in the state.

Torrington offers some of the best entry-level pricing in the state, paired with easy access to both rural amenities and regional commuting routes.

New Milford continues to draw buyers priced out of Fairfield County while staying within a reasonable drive of it — a common landing spot for buyers making the explicit trade of commute time for affordability.

Litchfield itself trades a bit more on character and lifestyle, with a slower-paced market that rewards patient buyers.

Financing note for Litchfield County: Property taxes here tend to run more manageable than in Fairfield or Hartford counties, which can meaningfully change your qualifying debt-to-income ratio. If you've been told you don't qualify for a certain purchase price in a high-tax county, it's worth running the same income against a Litchfield County property — the tax difference alone can shift what you're approved for.

New London and Windham Counties: Where USDA Financing Comes Into Play

Eastern Connecticut is the part of the state most buyers overlook, and it's also where a financing tool most banks barely touch becomes genuinely useful: USDA Rural Development loans, which allow eligible buyers to purchase with 0% down.

Norwich and New London offer some of the lowest entry prices in the state, with multi-family properties in particular showing strong fundamentals for buyers interested in house-hacking or investment potential alongside their primary residence.

Willimantic, in Windham County, sits squarely in USDA-eligible territory for many surrounding parcels — worth checking specifically before assuming you need a down payment at all.

Financing note for this region: Most retail banks don't actively originate USDA loans because volume here is lower than in conventional or FHA lending. A broker who works USDA financing regularly will move these files faster and know the eligibility maps better than a loan officer who only sees one or two USDA deals a year.

Connecticut Towns at a Glance

Town County Best For Financing to Ask About Hartford Hartford Equity growth, lowest entry cost in the metro FHA + lender DPA, grant programs West Hartford Hartford Walkability, schools Conventional, FHA New Britain Hartford Value with appreciation upside FHA + lender DPA Glastonbury Hartford Family-oriented, strong schools Conventional + PMI-waiver/grant stacking Stamford Fairfield Commuter access to NYC Jumbo, conventional Norwalk Fairfield Coastal commuter market Jumbo, conventional Greenwich Fairfield Luxury, long-term hold Jumbo, asset-based, non-QM Danbury Fairfield Fairfield County access at lower cost FHA, conventional New Haven New Haven Walkable, transit-connected FHA + lender DPA Milford New Haven Coastal value Conventional, FHA Cheshire New Haven Family living, mid-range pricing Conventional, FHA Torrington Litchfield Best price-per-square-foot in the state FHA, conventional New Milford Litchfield Fairfield County alternative Conventional, FHA Norwich New London Multi-family and investment potential FHA, conventional, multi-family financing Willimantic Windham 0%-down eligibility USDA Rural Development

Frequently Asked Questions

Is it cheaper to buy in Hartford or Fairfield County? Hartford County is significantly cheaper on entry price, and currently shows the fastest appreciation in the Northeast. Fairfield County costs more upfront but carries stronger long-term demand tied to its proximity to New York City.

Which Connecticut towns qualify for USDA 0%-down loans? USDA eligibility is determined by specific rural-area maps rather than county lines, but much of Windham County and parts of New London County fall within eligible zones. A loan officer who works USDA financing regularly can check a specific address against the current eligibility map in minutes.

Do I need a real estate agent and a mortgage broker, or can one person handle both? In Connecticut, mortgage origination and real estate brokerage are separate licenses, and they should stay that way — you want independent advice on both sides of the transaction. A good loan officer and a good local agent typically work as a team, not a single point of contact.

What's the fastest-appreciating town in Connecticut right now? Hartford currently leads not just Connecticut but the entire Northeast region in buyer equity advantage, driven by an appreciation rate above 11% annualized against still-reasonable entry pricing.

How to Actually Use a Town-by-Town List Like This

A few honest notes, because most "best towns" content skips this part:

Appreciation isn't the only thing that matters. Hartford's appreciation numbers are genuinely exceptional, but if your job, family, or life is centered in Fairfield County, commuting two hours a day to chase appreciation isn't a real plan. Use this guide to widen your search radius, not to override your actual constraints.

Out-migration is creating real inventory. A significant number of Connecticut homeowners have sold and moved out of state recently, and that's loosening up supply in several of the towns above — particularly across Litchfield and the eastern counties. That's part of why patient, well-prepared buyers have more negotiating leverage in 2026 than they did even two years ago.

The right loan program often matters more than the town. A first-time buyer in New Britain stacking FHA financing with a lender-offered down payment assistance program can end up with a lower effective cost of homeownership than a buyer in a "cheaper" town who's stuck with a standard conventional loan and no assistance. Town selection and loan structuring should happen together, not separately.

Pre-approval needs to match the market you're buying in. A pre-approval letter that worked fine in Litchfield County's slower-paced market may not be competitive in Stamford, where multiple-offer situations are common. Make sure your pre-approval is actually structured for the specific town you're targeting.

Bottom Line

There's no single "best town" in Connecticut — there's a best town for your specific financial picture, commute requirements, and what kind of loan program you can use. Hartford County currently offers the strongest pure equity play in the region. Litchfield County offers the best value and most negotiating room. Fairfield County remains the premium, high-demand option for buyers prioritizing commute and long-term appeal. New Haven County splits the difference. And the eastern counties hold financing tools — like USDA's 0%-down option — that most buyers don't even know to ask about.

Let's Find Your Town and Your Loan

I work with buyers across every county in Connecticut and stay close to which towns have active lender down payment assistance and grant programs, which qualify for USDA financing, and which lenders are actually competitive in each market. If you're trying to figure out where your budget actually goes furthest in Connecticut, that's exactly the conversation I have every day.

Geo Colon Senior Loan Officer, South Wind Financial (NMLS #MB9462) NMLS #1880655 | Licensed in CT, MA, RI 📞 617-821-1757 📧 [email protected] 🌐 loanswithgeo.com

This article is for informational purposes only and does not constitute a commitment to lend or a guarantee of future home value appreciation. Market data, loan program availability, and town-level eligibility (including USDA boundaries and lender-specific down payment assistance programs) change frequently and should be verified at the time of application. This article does not constitute real estate brokerage advice; consult a licensed Connecticut real estate agent for representation in a purchase or sale. Contact a licensed loan originator to confirm current mortgage terms. Equal Housing Opportunity.

Subscribe to my newsletter

South Wind Financial, Inc.

Mortgage Broker Lic #MB9462

Branch NMLS #86116

1356 Atwood Ave. Johnston, RI 02919

Stay Connected:

Privacy Policy | Terms of Services

© Copyright All Rights Reserved